When it comes to life, income protection and TPD insurance, there are several factors worth discussing with your financial adviser, as you may need to make trade-off decisions to keep premiums at an affordable level.

If you are paying too much in insurance premiums, there could be a number of reasons, including:

One often-overlooked factor that adds to the cost of cover is the percentage of commissions insurance companies pay to your financial adviser. These payments can have a direct impact on the premiums you pay. Removing this commission at the outset—particularly the “year on year” or ongoing trail commission—is comparable to a lifetime discount on your policy.

For this blog, policies that pay commissions have raised three major questions:

There is no legislative obligation for insurance policies to be reviewed. In fact, many clients report little to no ongoing service—just occasional administrative help. This has allowed advisers to respond only when required or when clients raise concerns about premium affordability, but this usually happens a few years into the policy. Contact after two years also presents another opportunity for advisers to sell a replacement policy and collect another upfront commission.

This blog compares insurance premiums with vs without commissions, and questions whether you should seek advice from an adviser who does NOT accept these payments—such as an Independent Financial Adviser, who is instead remunerated on a Fee-For-Service basis.

The following case study is an example only. It is based on a live quote from a reputable insurance provider; however, as people and policies differ, the conclusions highlighted are not reflective of all situations.

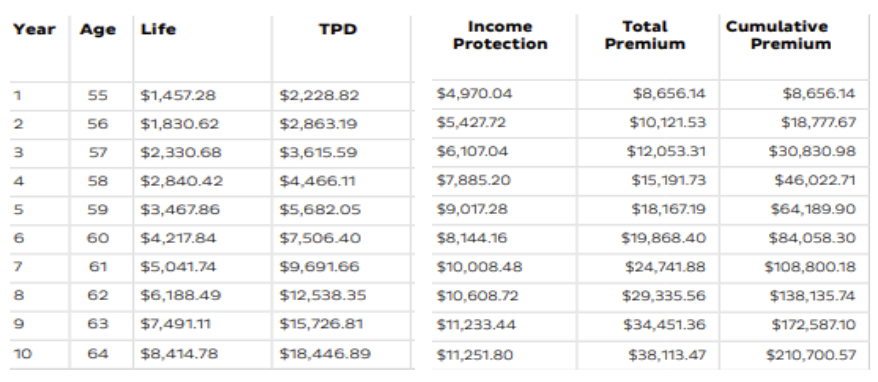

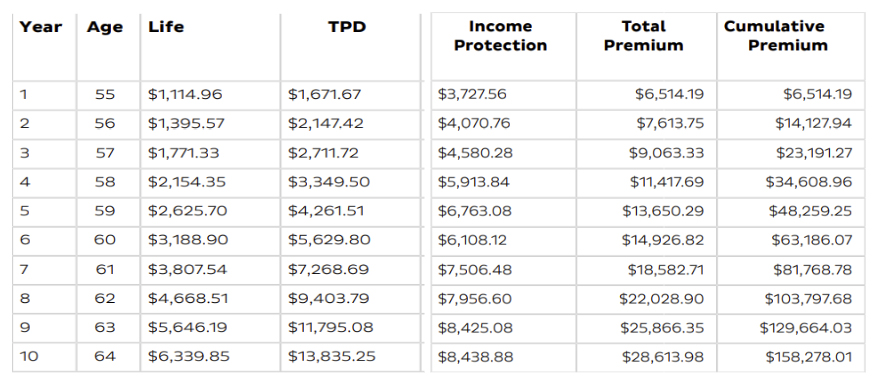

Premium comparisons are based on the current standard ‘Hybrid’ commission rates being accepted in full, i.e. 66% in Year 1 and 22% in Year 2+.

Note: Commission is not payable on the policy fee, stamp duty and modal/frequency loading for monthly or quarterly premium payments. The commission rates are inclusive of GST.

Most clients do not refer back to their original Statement of Advice or Fee Disclosures to recall how much remuneration their adviser is receiving in ongoing trail commissions. In most cases, clients are unaware that they have been directly funding these commissions through premium payments. Many are also unaware of what services they are entitled to, or may simply not need annual support services.

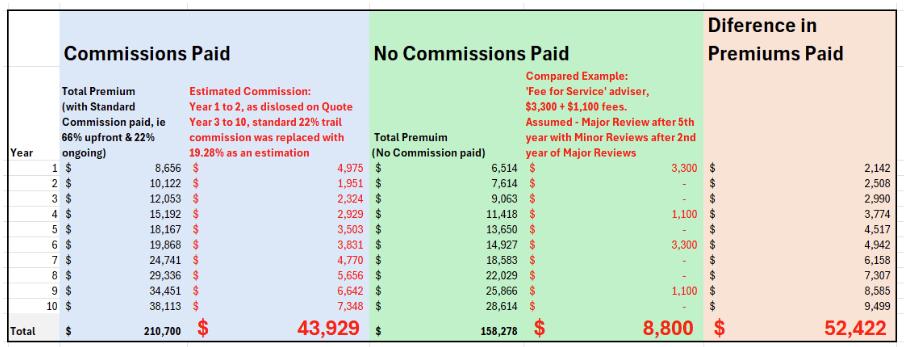

As seen in the table, the difference in premiums over time is large, and the commission (representing adviser remuneration) is paid regardless of whether service is provided.

If commissions were removed, the resultant discount and savings in premiums would be significant. Even if the Fee-For-Service was increased above $3,300 plus $1,100 for periodic reviews, it is unlikely to exceed standard commissions paid.

Review frequencies are typically not required every year. With ‘stepped’ premiums, it is generally known that premiums will rise annually. Clients generally only contact their adviser when their circumstances change—such as taking on extra debt, welcoming a new child, or when premium affordability becomes an issue.

By law, there is no obligation for advisers to review insurance policies. While many advice firms may, as a courtesy, offer annual review opportunities to clients, the majority do not take up this offer. Insurance providers will also contact policy owners prior to an anniversary to notify them about updated premiums and cover for the next 12 months. Most clients should be aware of what they are paying in premiums.

Under Fee-For-Service, the adviser is paid a fixed fee for work performed, much like a contractor or lawyer. Usually, this fee is for the initial research and documentation of advice (Statement of Advice). Implementing your insurance is typically included in this cost but may sometimes be a separate fee.

The charging of fees should reflect:

In later years, if you need a ‘Review’ or subsequent advice, a separate fee will be discussed and charged according to the requested work. Separate fees may also apply to administrative support or claims support; however, these services are often better sourced directly from the insurance provider. With claims support especially, the insurance provider’s specialist team will ultimately approve or decline the claim.

Under Fee-For-Service, there is no ongoing obligation for the adviser to review or provide services unless specifically agreed to.

Possible reasons include:

Data from Quotes used in Case Study:

Applicant:

Cover: